When a family member, tenant, employee, or resident has just been found in distressing circumstances, their minds aren't thinking about policy language or claim forms. They're thinking about privacy, safety, and what needs to happen in the next hour. Property managers may be trying to secure a unit before other residents notice. Families may be standing outside a home, shaken, wondering who to call first.

That's where insurance billing services matter, but not in the abstract. In trauma cleanup, billing support is part of crisis support. Someone still has to document the loss, explain the scope of work, speak with the carrier, and make sure the claim reflects what transpired at the scene.

In my experience, people get overwhelmed for two reasons. First, the event itself is emotionally heavy. Second, insurance sounds simple until you're the one trying to answer an adjuster's questions about contamination, disposal, and whether the loss falls within the policy. A capable remediation partner helps carry that burden so you can focus on the people involved, not just the paperwork.

Navigating a Crisis with an Expert Partner

A common call goes like this. A daughter has discovered that her father passed away alone in his apartment. A property manager is worried about neighboring units. Nobody knows whether the cleanup is covered, who approves the work, or what the insurance company will need before payment is even considered.

In that moment, “insurance billing services” shouldn't mean a stack of forms dropped on a grieving family. It should mean calm coordination. It should mean someone explains what happens first, what documents matter, and how the carrier usually reviews a trauma-related claim.

Specialized billing support has become a major part of the broader insurance ecosystem. The global medical billing outsourcing market was estimated at $14.90 billion in 2024 and is projected to reach $44.30 billion by 2033, showing how vital specialized billing partners have become, according to medical billing industry statistics.

What families and managers usually need first

The first need is clarity. People want to know whether they should call the carrier before cleanup starts, whether an adjuster must inspect the site, and whether they're allowed to authorize emergency work.

The second need is advocacy. Many readers don't realize the insurance company may assign its own adjuster, while policyholders can also seek independent guidance. If you're trying to understand that difference, this plain-language guide on public adjuster vs company adjuster is useful before major claim conversations begin.

What a strong remediation partner does

A professional team doesn't just remove contamination. It helps stabilize the situation so the claim has a clean foundation.

Practical rule: The earliest decisions often shape the entire claim. If the scene is documented poorly or handled by the wrong vendor, the billing dispute starts before cleanup is finished.

That's one reason many families look for a provider that can manage both emergency response and insurance coordination. Guidance on why calling a professional cleanup team first can protect the process often helps people understand why the first phone call matters so much.

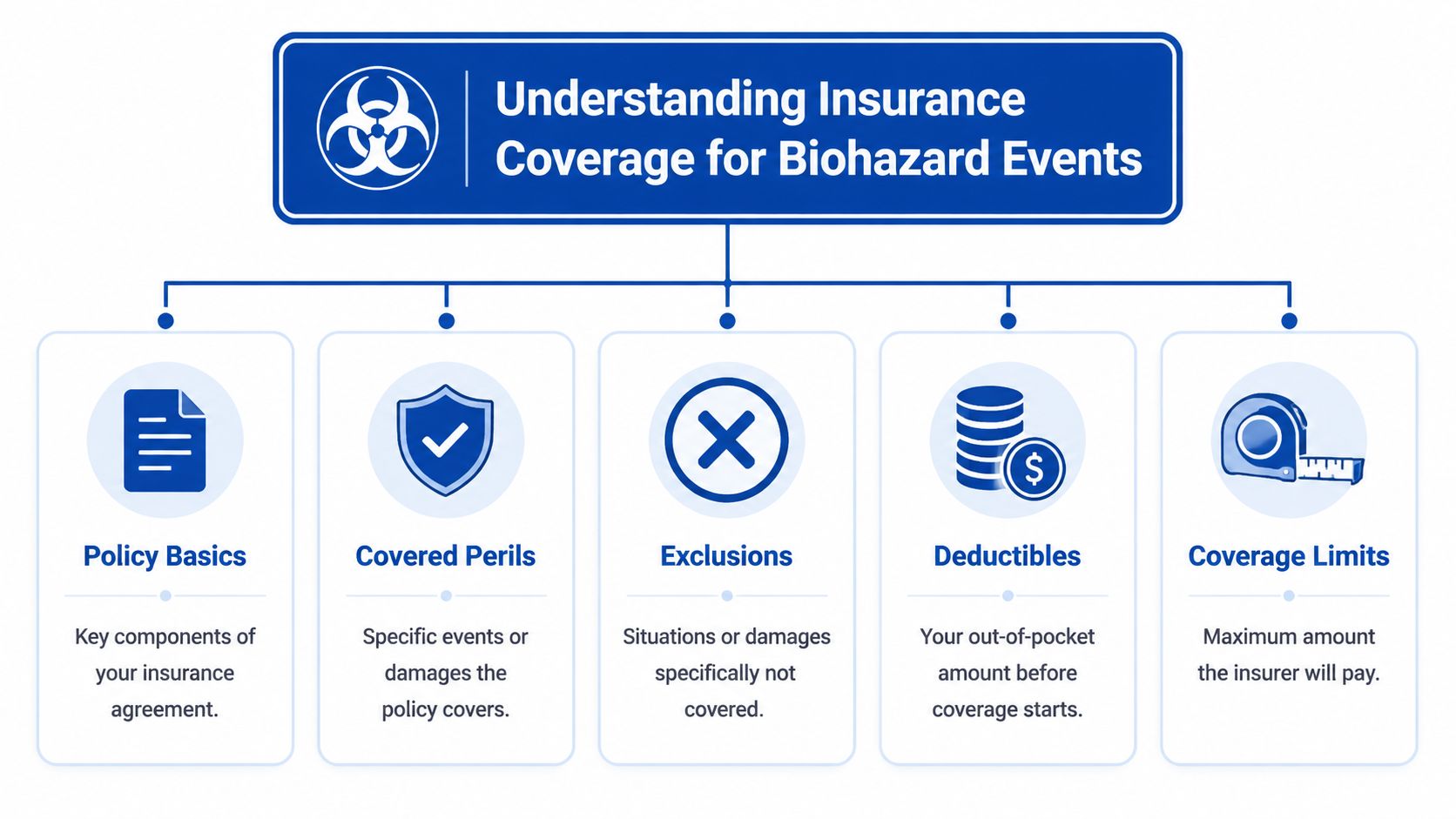

Understanding Insurance Coverage for Biohazard Events

Insurance policies can feel like legal puzzles when you're already under stress. I prefer a simpler way to think about them. A policy is a financial first-aid kit. It may help with certain losses, but only if the event fits the policy, the documentation is solid, and the cost stays within the limit set by the contract.

That's why the first coverage question isn't “Will insurance pay?” It's “What kind of event caused this contamination?”

What policies often cover

For many homeowners, landlords, and commercial property operators, biohazard cleanup may fall under the part of the policy that addresses damage tied to a covered event. Standard homeowners and commercial policies typically cover biohazard cleanup under dwelling or personal property sections for crime-related incidents and accidental trauma, with coverage limits ranging from $5,000 to $50,000 depending on policy terms, as outlined in this overview of biohazard cleanup cost and insurance coverage.

That doesn't mean every scene is automatically approved. The carrier still looks at cause, timing, policy language, exclusions, and proof that the work performed matched the actual contamination.

Five policy terms that confuse people most

- Covered peril means the kind of event the policy agrees to insure. In this context, that might include a crime-related incident or accidental trauma.

- Exclusion means a situation the policy specifically leaves out.

- Deductible is the amount the policyholder is responsible for before insurance contributes.

- Coverage limit is the most the insurer will pay under that part of the policy.

- Claim number is the file identifier the carrier creates so all documents, invoices, and communications attach to the same loss record.

If you don't know whether the event fits a covered peril, don't guess. Ask the carrier how they're classifying the loss and write down the answer.

A simple way to read your next conversation with the carrier

When you speak with the insurer, try to sort the discussion into three buckets:

Cause of loss

What happened at the property, and is that event normally covered?Scope of contamination

Which rooms, contents, surfaces, or systems were affected?Financial limit

What part of the policy applies, and how much room is left under that limit?

Families often need a straightforward explanation of who typically pays in these situations. This article on who pays for crime scene cleanup can help frame that conversation before you authorize work.

The Critical Role of Professional Remediation

A trauma scene isn't a janitorial problem. It's a health, safety, and documentation problem. That distinction matters to families, but it matters just as much to insurance carriers.

If untrained people clean a scene, they can spread contamination into hallways, HVAC systems, furnishings, and adjacent rooms. They can also destroy the very evidence the insurer needs to evaluate the claim. Once that happens, the argument about payment gets harder because the record is incomplete.

Why regular cleaning isn't enough

Biohazard scenes involve bloodborne pathogen risk, controlled handling, personal protective equipment, and regulated waste disposal. A standard house cleaner or maintenance crew usually isn't equipped to manage those hazards, and they shouldn't be asked to.

OSHA mandates under 29 CFR 1910.1030 that every employer with potential exposure risks must create and annually update a written Exposure Control Plan, making professional, documented biohazard remediation a regulatory necessity, as explained in OSHA guidance for biohazard cleanup.

Why insurers care how the work is performed

Carriers don't just evaluate the invoice amount. They look at whether the work was necessary, whether the vendor followed recognized procedures, and whether the record supports the scope charged.

A professional remediation team typically brings several things a non-specialist can't:

- Scene-specific hazard controls that limit cross-contamination.

- Documented work practices that show what was removed, cleaned, disinfected, and tested.

- Proper waste handling so disposal can be traced and verified.

- A defensible scope of work that aligns cleanup actions with the actual loss.

Cleanup done without proper controls can create a second loss. The insurer may then question which damage came from the original event and which damage came from improper handling.

What families and facility managers should ask

Before authorizing any company, ask practical questions:

- Who will document the scene for the insurance file?

- How will contaminated materials be tracked and disposed of?

- What safety plan governs the crew's work on site?

- Can the provider explain the scope in plain language to an adjuster?

Those aren't technicalities. They're the difference between a clean, supportable claim and a confusing one.

How 360 Hazardous Coordinates Your Insurance Claim

When people hear “insurance coordination,” they often imagine a few phone calls and an invoice sent later. In reality, proper coordination starts at the first conversation and continues through documentation, carrier communication, and settlement review.

One option families and property managers use is insurance claim help for biohazard cleanup, where the remediation company works alongside the policyholder and carrier rather than leaving the client to organize everything alone.

What coordination looks like in practice

The process usually begins with an initial assessment. The team identifies affected areas, immediate safety concerns, and what must be documented before work begins. At that point, the claim file needs structure, not just urgency.

After that, the workflow often includes:

Claim filing support

The client gets help gathering the basic facts the carrier will ask for, including the date of loss, type of incident, and policy information.Evidence collection

Photos, incident details, disposal records, and scope notes are organized so the insurer can follow the logic of the bill.Adjuster communication

The remediation side explains what contamination was present and why specific work steps were necessary.Estimate review

The scope is matched to the affected materials and conditions on site.Billing follow-through

If the carrier asks for clarification, supplemental material, or revised line items, someone responds with supporting records rather than vague explanations.

For readers who want a broader property-claim primer, especially in a residential context, this Guide to Miami property claims offers a helpful overview of how claim filing conversations usually unfold.

A short walkthrough can also make the process easier to picture:

What clients should expect from the billing side

Strong insurance billing services should feel organized and humane at the same time. You should know who is speaking with the carrier, what documents have been sent, and whether the insurer has requested anything else.

That means a good coordinator should be able to answer questions like these without making you chase updates:

- Has the claim number been issued?

- Did the adjuster receive the photos and estimate?

- Are they questioning scope, coverage, or pricing?

- Is any family or property representative signature still needed?

When those answers are clear, the whole situation becomes more manageable.

Essential Documentation for a Successful Claim

Most claim delays come from one problem. The carrier can't see a clean chain from the event to the work performed and then to the charges billed. Documentation exists to build that chain.

Insurance billing for biohazard remediation relies on the industry-standard ANSI/IICRC S540 protocol, which mandates specific documentation like project assessment maps and post-job testing reports to satisfy carrier requirements, as explained in this review of biohazard contractor insurance and S540 documentation.

What the carrier is trying to verify

An adjuster typically wants to answer four questions:

- Was this a covered event?

- How far did contamination extend?

- What work was necessary to return the property to a safe condition?

- Do the charges match the documented scope?

That's why a claim file needs more than a final invoice. It needs a record of what was found, what was done, and what was lawfully disposed of.

Key documents for insurance claims

| Document Type | Purpose for the Insurance Carrier |

|---|---|

| Claim number and policy details | Connects all records to the correct loss file and verifies the policy in effect |

| Scene photographs | Shows visible conditions before work and supports the contamination narrative |

| Professional estimate | Translates observed conditions into a defined scope of remediation |

| Project assessment maps | Identifies affected areas and helps justify room-by-room or material-specific work |

| Itemized invoice | Links labor, equipment, materials, and disposal to actual remediation tasks |

| Disposal manifests | Verifies regulated waste handling and lawful disposal |

| Post-job testing reports | Demonstrates the site reached the required decontamination endpoint |

| Police or incident reports, when applicable | Supports cause of loss and helps establish whether the event fits a covered peril |

Why chain of custody matters

Families are often surprised that disposal paperwork matters so much. But once contaminated materials leave the property, the insurer may still want proof of what was removed and where it went. That's part of making the bill auditable.

For a closer look at how evidence and waste records should be preserved, this overview of chain of custody procedures is worth reading.

The cleanest invoice in the world won't carry a claim by itself. The supporting record has to show why each charge belongs there.

A practical checklist before submission

Before records go to the carrier, confirm that the file includes:

- A clear cause-of-loss record that matches the policy claim.

- Before-work images showing the affected conditions.

- A defined scope that identifies all contaminated areas.

- Line-item billing tied to the work performed.

- Final documentation showing disposal and completion.

That level of discipline protects the client as much as the vendor.

Navigating Common Billing Pitfalls and Complexities

Many people assume the hardest part is getting the claim opened. Often, the harder part comes later, when the carrier questions scope, applies an exclusion, or pays less than expected without fully explaining why.

That's when clients feel blindsided. They thought cleanup was the emergency, but now billing has become the stress point.

Where claims often go sideways

Some disputes are straightforward. The deductible applies, a document is missing, or the policy limit is lower than the invoice total. Others are murkier. The insurer may agree that the event happened but challenge whether all affected materials had to be removed, sealed, or disposed of.

Property managers and families should slow the conversation down and ask the carrier to identify the exact basis for any reduction:

- Is the issue coverage?

- Is the issue scope of work?

- Is the issue documentation?

- Is the issue a policy limit?

Those are very different problems, and they require different responses.

The No Surprises Act question

A more complex issue involves federal billing protections. A key complexity is the lack of clear guidance on how biohazard cleanup fits within the “emergency services” protections of the No Surprises Act, which can lead to unexpected balance bills that clients may have grounds to dispute under CMS guidance on surprise medical bills.

That doesn't mean every trauma cleanup bill is covered by those rules. It means the boundary isn't always obvious, especially when services are connected to emergency conditions or facility-based care. If a family receives an unexpected bill after urgent contamination response, it's reasonable to ask whether any CMS dispute pathway or related billing protection may apply.

Ask for the legal basis, not just the billing result. If someone says a charge is your responsibility, ask which policy provision or rule they're relying on.

How to respond without making things worse

If you think the billing outcome is wrong, don't rely on a verbal summary from a call center. Request written confirmation of the carrier's position. Then compare that position to the estimate, scene record, and policy language.

This guide on how to talk to your insurance company about cleanup services can help clients keep those conversations focused and productive.

A calm challenge is often more effective than an emotional one. Ask narrow questions. Request written explanations. Keep every document.

Frequently Asked Questions About Insurance Billing

Will filing a biohazard cleanup claim raise my premiums

It might, but your policy and claim history matter. The better question in a crisis is whether the event is covered and whether you can document it correctly. Families shouldn't avoid reporting a legitimate loss just because they fear an outcome the carrier hasn't even evaluated yet.

Who pays the deductible

In most cases, the policyholder pays the deductible. The insurance company then pays covered amounts above that threshold, subject to the policy's terms and limits.

What if the claim is denied

Ask for the denial in writing and read the reason carefully. Some denials turn on missing records or unclear cause-of-loss descriptions rather than a final determination that no coverage exists. If the explanation doesn't make sense, gather the estimate, photos, and incident records and ask for a formal review.

Can a remediation company bill insurance directly

Sometimes, yes. The exact setup depends on the carrier, the policy, and the service agreement. What matters most is that the billing is transparent, documented, and tied to the approved or supportable scope.

What should I keep in my records

Keep every email, estimate, invoice, photo set, claim number, and disposal record. If the insurer asks questions later, the ability to produce a complete file matters more than memory.

Is biohazard billing similar to medical billing

There are similarities in the sense that both require disciplined documentation, payer communication, and clean billing logic. If you want a broader non-remediation example of how structured reimbursement systems work, this overview of optimizing healthcare RCM gives useful context for why specialized billing support exists at all.

What's the best next step if I'm overwhelmed

Write down the claim number, the adjuster's name, and the exact event date. Then ask for a written list of anything the carrier still needs. A stressful claim becomes much easier to manage once the open questions are visible on paper.

If you're dealing with a trauma scene, unattended death, crime scene, or other biohazard event and need clear help with cleanup documentation and insurance communication, contact 360 Hazardous Cleanup. Their team provides biohazard remediation and can coordinate with carriers so families, facility managers, and property owners have a safer, more organized path forward.